Wunderman Thompson and Dattel Unveiled Findings from A Survey of Thai People’s Purchasing Behaviours During COVID-19

The new survey finds Thais most worried in APAC about COVID-19 impact on the economy, resulting in changes in purchasing behaviours. Wunderman Thompson urged brands to turn crisis into opportunity by building consumer loyalty during the pandemic for business viability and brand salience in the future.

15 APR 2020, Bangkok – While people and business sectors around the world have yet to come to terms with coronavirus disease 2019 (COVID-19), the pandemic has triggered significant changes to the decision-making of consumers, who are being affected by its social, mental, and economic impacts. For a more insightful understanding of consumers, Wunderman Thompson and Dattel have conducted a nationwide survey from March 24 to 26 to study behavioural changes of Thai consumers during COVID-19 outbreak and beyond. The study covered 1,243 respondents aged between 15 and 69 years old in Bangkok and upcountry, 32% of whom are male and 68% female with education levels ranging from mid-school to doctorate degree. It dived deep to understand their behaviours in 3 core segments: low involvement, high involvement, and retail & services. For numerous reasons, the behaviours differ between groups of consumers and categories, and while some categories are heavily affected, the impacts on some others are minimal. Brands should, therefore, understand these behaviours to ensure their viability during and after the crisis.

Maureen Tan, Chief Executive Officer of Wunderman Thompson Thailand, said, “All of us are facing with an unprecedented situation as COVID-19 is posing a global threat to consumers, businesses and disrupting industrial and business operations across the world. The survey we conducted together with Dattel delved deep into consumer behaviours before, during and after COVID-19 to provide brands and companies with the market insights they would need for better business planning and decisions in this time of crisis.”

“Wunderman Thompson Thailand has actively supported our vision and mission since the beginning,” added Ashran Ghazi, Chief Executive Officer of Dattel Group. “We are very excited to be part of this collaboration by providing valuable consumer insights. Our expertise is based on holistic consumer data, which makes it possible to identify and capitalise on the behaviours of consumers who are affected by COVID-19 pandemic. Moreover, we have an edge of strong cohort analysis as our source of consumer intelligence across behaviours and attitudes.”

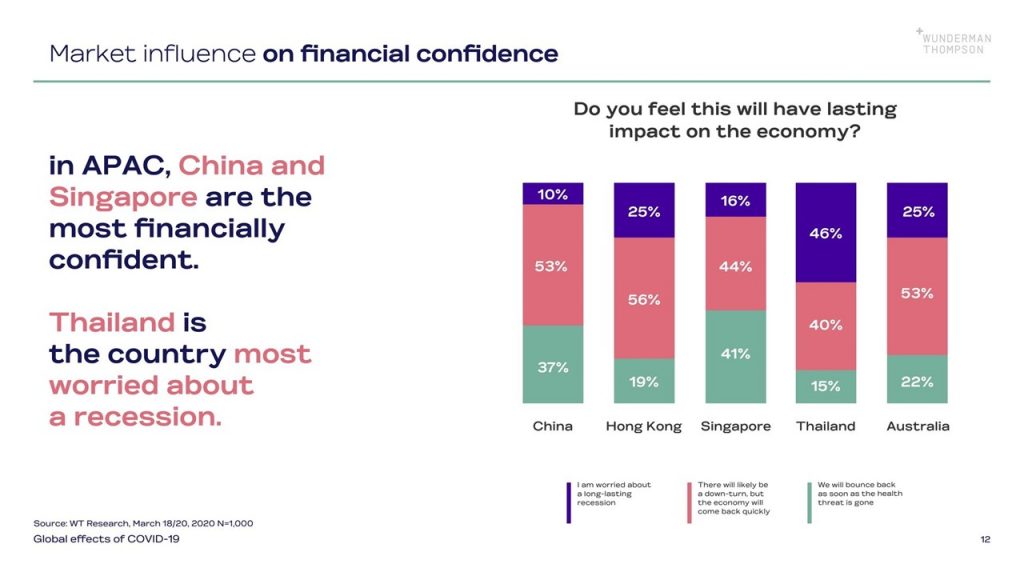

Thailand Is the Most Worried Country in APAC When It Comes to Economic Impact

Wunderman Thompson has been conducting a series of surveys on the impacts of COVID-19 in China, Hong Kong, Thailand, Singapore and Australia to collect data and track changes in consumer behaviours. The study found three-fourths expecting a recession or downturn. It also unveiled a heightened level of concern linked to social media consumption in all the countries, led by Australia with 43% of respondents who are concerned about COVID-19 contraction, followed by Thailand (14%), Singapore (13%), Hong Kong (8%) and China (3%). Meanwhile, all media types have seen dramatic increases in consumption, including social media, news programmes, online meetings, terrestrial/digital TV, streaming programmes, online gaming, streaming music, books, newspaper and podcasts. In the Asia Pacific, China and Singapore are the most confident that the economy will bounce back as soon as the health threat is gone. In contrast, Thailand is the most worried about a recession—only 15% of Thai respondents believe that the economy will recover quickly after the outbreak.

With increased concern, the behaviours of Thai consumers have changed. Wunderman Thompson and Dattel have therefore surveyed consumer’s purchase behaviours and decisions pre, during and post COVID-19 to study the depth of its impacts on three core segments: low involvement, high involvement, and retail & services.

Low Involvement: Increased purchase volume and pack size in grocery and household categories

Low involvement categories are, for example, food and beverages, health and beauty, and house and household. In terms of purchasing channels, the most popular venues that consumers shopped pre-COVID-19 were offline, with convenience stores far higher than other channels at 76%. During COVID-19, consumers with monthly income below 30,000 baht indicated a higher chance of visiting offline channels less often or stopping altogether. For convenience stores, however, about half said the frequency remained the same or more often during COVID-19. In contrast, consumers with incomes higher than 30,000 baht a month indicated that their purchases would be the same or more during this period, and they are also more likely to maintain or increase their online purchases. Food & beverages are safe from COVID-19 as the majority of consumers indicated that they would either maintain or increase the purchase volume, pack size, and spend. Instant noodles see the most significant increase with 52%, showing their increase in purchase volume. Health and beauty category will remain relatively unchanged during COVID-19.

Over-the-counter medicine sees the most significant likelihood of increased capacity, pack size, and spend as indicated respectively by 32%, 17% and 28% of the respondents. Cosmetics will be mostly stable, but also has the highest chance to see a decline across spending and purchase volume. Household goods are the least affected group. Laundry care and facial tissues see the highest likelihood for increased capacity (29% and 24%), increased pack size (18% for both products) and increased spend (24% and 22%). When asked about post-COVID-19, the majority of consumers have a pessimistic outlook, saying that they would either visit shopping venues less or stop altogether. Uncertainty of the future and income contributes to consumers’ anticipation that they will reduce their shopping habits. The study also covered brand preference and loyalty. It found that most consumers have a brand in mind before purchasing. The most influential brand preference can be seen in the toilet/facial tissue products, as suggested by 75% of respondents. In contrast, vitamins/supplements have the least brand preference at 47% (beer and pet care excluded due to inapplicability to many respondents). Haircare and facial care brands have the highest loyalty (67% and 69% respectively), while snack food, instant noodles and bakery have the highest likelihood for brand switching.

What Brands Can Do

- Since consumers have indicated their desire to continue or even increase purchasing behaviour in low involvement categories, it will be unwise to slow down or stop marketing efforts no matter online or offline. It is essential to keep your brand presence strong in the media space and invest in building lasting relationships with consumers to assure top-of-mind awareness and pave the way for brand loyalty.

- Offline presence needs to remain steadfast in support of product availability and purchasing decisions across all channels. Rather than lowering their prices, brands should consider offering consumer bundle packs at reasonably discounted prices to drive volume.

- Along with the development of a more robust e-commerce presence, brands should ensure that all forms of communication contain strong calls-to-action to buy online. Consider adding free delivery or buy one, get one free promotion in e-commerce to drive bulk purchasing.

- Most consumers have a brand in mind, but when it comes to purchasing, close to a third switches brands. It is worth going back to basics on activating the consumer journey with the right content, right time, right channel. Besides, investing in media that build brand salience and optimise your media mix. From consumers’ point of view, talk about why your products are great: this is not about how great you are; it is about how great you can help consumers improve their lives.

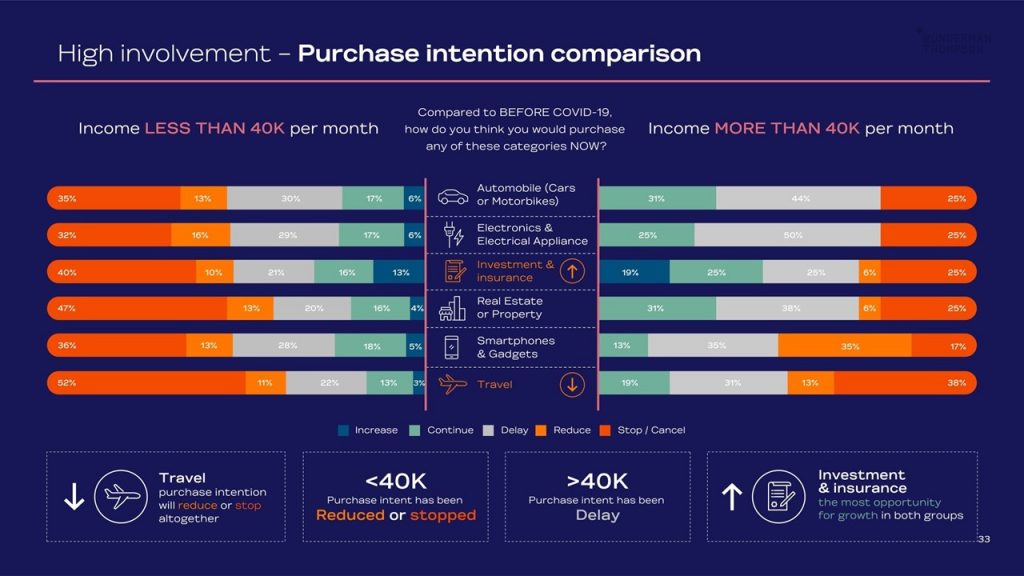

High Involvement: Necessity is the most significant influencing factor for those with monthly income below 40K versus return on investment (ROI) for those who earn more than 40K per month

High involvement categories are, for example, automotive, real estate and property, electronics and electrical appliances, smartphones and gadgets, investment and insurance, and travel. During COVID-19, purchase intents have declined in all categories, but investment and insurance showed a relatively higher chance of consideration. Among those earning more than 40,000 baht a month, categories with the most significant reduction in comparison to pre-COVID time are auto and electrical appliances. As for post-COVID-19 reconsideration of delayed, reduced or cancelled purchase intents, consumers with sub-40,000-baht income are more likely to sideline their intentions indefinitely. In contrast, those who earn more than 40,000 baht tend to reconsider purchasing in all categories within periods from one month up to more than one year after COVID-19.

Automotive has a high chance for a post-COVID-19 rebound in 3 – 6 months as indicated by 55% of the 40K+ income group, which also show the quickest period of 1 – 3 months to reconsider purchasing electrical appliances, smartphones and gadgets, and travel (8% across all these three categories). On influence and loyalty fronts, the study found that necessity is the most significant decision influence on consumers with sub 40K income as indicated by 57% of this group. In essence, their limited spending power results in hesitation to consider high-involvement categories as a whole. Moreover, 52% of them do not have a preferred brand, but once they choose, they will most likely stay loyal (52%) to their preferred brand to avoid the risk of trying something unfamiliar. For consumers with monthly income above 40K, the biggest influencing factor is the return on investment as indicated by 80% in this group, in which the majority (69%) already has a brand in mind at the time of purchase consideration and show even more loyalty (56%) than the lower-income group.

What Brands Can Do

- While automotive is the category most affected by COVID-19, it is also most likely to rebound the fastest. Automotive brands need to treat this time as an opportunity to build positive brand perception to win consumers’ top-of-mind awareness once things go back to normal and ultimately be the chosen brand in their next purchasing decisions. Investment and insurance category should use their expertise to add value to consumers, who are now more concerned about their finances and future than ever before.

- Different groups of consumers need different influences on the messages they receive from brands. For the lower-income group, brands need to show why a product/service is needful and how it adds value that they cannot live without it. For the higher-income group, brands need to show how they are getting a worthy return on their investment.

- Once a high involvement brand can win a consumer over, they will most likely stay loyal, regardless of which group they are.

- For categories with affected sales in stores or closed on the ground in Thailand, e-commerce/online channels need to be strongly activated. Ensure you have a strong online/e-commerce presence that you can nurture and push lower value/range of SKUs to stimulate purchase as consumers are careful with spending.

- Nurture intenders and short-term delayers who have the intent to purchase by maintaining or increasing share of voice, especially online. Go more targeted and personalised—nurture intenders who visited your websites by doing more in-depth analytics on-site visits and capturing lead information through marketing automation to push them down the purchase funnel to conversion. Close the gap of consideration with promotional schemes such as instalment payment, 0% interest, or price-off deals.

- Start planning ahead for post-COVID-19 recovery plan.

Retail & Services: Grocery stores and petrol stations see the smallest impact

Retail & Services category includes grocery and sundry, food outlets, entertainment and leisure, beauty and drug stores, petrol stations, amongst others. On the frequency of visits to these venues before and during COVID-19, an overall decline is seen, but grocery stores and petrol stations see the smallest drops of -8.3% and -13.2% whereas entertainment, lifestyle venues, and restaurants experience the biggest declines of -60.8%, -58.1% and -56.5%, respectively. In terms of spending, both groceries and petrol stations see the highest share of consumers saying that they will spend more or stay the same before and during COVID-19. However, these two categories are highly volatile as each of them also has a large portion of consumers who indicated that they would spend less. Other categories see the spending decline significantly or stopping altogether. Post-COVID-19, most consumers say will likely return to their average level of spending before COVID-19. In particular, consumers indicated that their spending and visits to supermarkets, department stores, petrol stations, beauty and drug stores, entertainment and leisure, and health and active lifestyles would increase (18%, 10%, 9%, 8%, 7% and 7%, respectively).

What Brands Can Do

- Brands need to drive loyalty to keep consumers spending regularly and find ways to prevent them from spending less.

- With fewer consumers willing to go out, restaurants, entertainment and leisure, and lifestyle/health venues will need to shift their focus to maintain business and profitability. For example, restaurants may have to prioritise home delivery and cleanliness; movie theatres will have to stream movies online for a fee; bars and pubs can stream concerts online, set up virtual bars and home-delivery unique cocktails.

- There is not much that beauty and drug stores, department stores, and lifestyle/health can do during COVID-19. However, since these services often share physical space in close proximity, they should band together to plan for what will happen after COVID-19. They can begin offering special discounts for members of each, pooling media resources together to drive foot traffic, and implementing CSR campaign that helps employees during these uncertain times.

While the future remains uncertain as to when this situation will end, brands need to be readily adaptable with flexibility. The study of consumer behaviours in Thailand during COVID-19 exposed different purchasing behaviours in various categories, and even in one same category, the behaviours can vary by consumers’ income. Brands must understand these to win top-of-mind awareness after the outbreak. In retail and services, although groceries and petrol stations see the smallest impacts, consumer loyalty is still crucial to ensure a continuingly strong base of customers, their visit frequency and spending. Overall, FMCG brands do not see a significant impact during COVID-19. It is suggested that as consumers are stocking up, so ensure your brand maintains top-of-mind recall through consistent communication, creation of innovative services, as well as convenience and safety of consumers in this period to keep your revenues healthy across offline channels.

High involvement categories see the most significant decline in consideration during COVID-19. Brands should tailor their communications to different groups of consumers, focusing on return on investment for higher-income audience and necessity for low-up to middle-income groups. At the same time, they should utilise digital to nurture intenders and bring delayers back down the purchase funnel. Moreover, with social distancing policy put in place by the government, consumers are spending more time online than ever before. It is an ideal opportunity for brands to reach their consumers on digital platforms as they are online and receptive during times when they previously would not have been. With an insightful understanding of consumer behaviours and timely adaptation to changes, brands can turn a crisis into opportunity, generate revenues continuously and win consumer loyalty now and beyond the end of the outbreak.